The second quarter of 2025 presented a dynamic market environment. April began with a surprise tariff announcement that initially unsettled markets and sparked a sharp pullback. Concerns about economic growth emerged as early GDP readings turned negative and bond markets showed signs of stress.

However, the tone shifted in May and June as inflation moderated, job growth remained steady, and corporate profits surprised to the upside. Markets proved resilient in the face of ongoing policy uncertainty and geopolitical headlines.

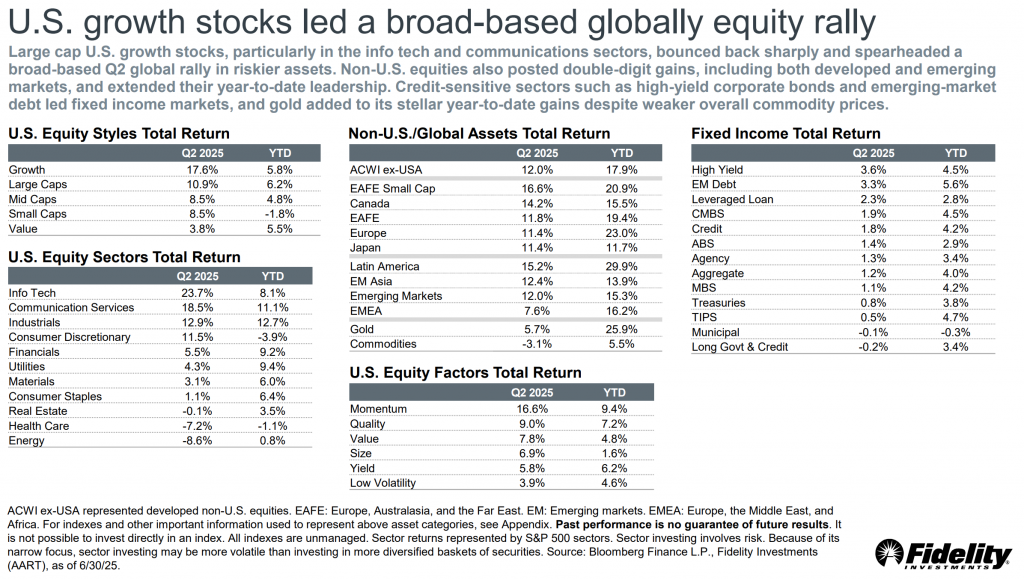

While clear signals were hard to come by this quarter, diversification continued to do what it does best: quietly manage risk when everything else is in flux.

Key Themes of Q2 2025

- Tariffs Took Center Stage

- April’s surprise tariff package triggered immediate market volatility and a surge in recession concerns.

- Tariff implementation was paused for 90 days (except for China), calming markets temporarily, but the uncertainty lingered.

- By June, a temporary agreement with China to lower reciprocal tariffs created a short-lived relief rally, although longer-term clarity remained elusive.

- The Fed: On Hold and Under Pressure

- Powell emphasized the need for more data and signaled the Fed would not pre-emptively cut rates to soothe markets.

- Inflation trended lower across the quarter, but stronger-than-expected labor data and mixed GDP signals kept the Fed cautious.

- Market-based expectations for rate cuts shifted from summer to fall, with September now seen as the most likely start.

- Inflation Continued to Ease

- CPI dropped to 2.3% in May and ticked up slightly to 2.4% in June, well below prior levels and close to the Fed’s 2% target.

- Businesses appeared to be absorbing higher import costs, avoiding price hikes to consumers—for now.

- Labor Market Held Firm

- Payrolls beat expectations all quarter:

- April: +177K

- May: +139K

- June: +147K

- Unemployment hovered around 4.2% before dipping slightly to 4.1% in June, supporting the case for economic resilience.

- GDP and Business Activity Softened

- Q1 GDP came in negative (-0.3%), primarily due to a massive 41.3% surge in imports as companies stocked up ahead of tariffs.

- The Fed downgraded its GDP outlook:

- 2025: From 1.7% → 1.4%

- 2026: From 1.8% → 1.6%

- Consumer and Housing Market Showed Signs of Strain

- Consumer confidence plunged in April and rebounded only slightly before turning negative again in June.

- Housing flipped from a seller’s to a buyer’s market:

- Mortgage rates topped 7% before easing.

- Sellers now outnumber buyers by 34%—the widest gap in 12+ years.

For those looking for more detail, here is a link to a video by David Kelley, Chief Global Strategist at JP Morgan Global Asset Management.